Bitcoin has been criticized by mainstream economists and financial institutions for many years. It has been repeatedly attacked by authoritative figures, yet it has continued to reach new highs.

Recently, Bitcoin’s price has once again been rising steadily. Many traditional investors are hesitating over whether they should buy Bitcoin. The most common questions include: Is Bitcoin really a currency? Does it have any intrinsic value? Given how high the price already is, how much further can it rise?

This article attempts to answer these questions.

Disclaimer: This article is intended for traditional investors with mature investment experience in financial markets, and assumes that readers already understand the basic operating mechanism of Bitcoin.

Traditional Money

Economists’ understanding of money has gone through several stages, each based on the forms of money that had already become widely accepted in human society.

In the era of Adam Smith and Karl Marx, money was understood first and foremost as a commodity — something that had the attributes and value of a commodity itself.

This conclusion was mainly based on the historical records available at the time. For example, people used gold, silver, copper, iron, and other metals as money. These things were first commodities with practical use value. Second, they were convenient to store, carry, and measure; difficult to reproduce; and relatively scarce. Therefore, they were suitable to be selected as money.

This type of money was understood as a medium of exchange serving as a general equivalent. For example, if one tael of silver could buy one ice cream, that meant the commodity value of the ice cream was equivalent to the commodity value of the silver.

Adam Smith

This concept effectively lasted until the gold-standard era of the twentieth century. At that time, money could be rigidly converted into gold. So, at least nominally, it was still money based on commodity value, even though in reality governments had long since printed far more paper currency than could be rigidly redeemed for gold.

It was not until the collapse of the Bretton Woods system in the 1970s, when the dollar was decoupled from gold, that money became the fiat money we use today. Only then did economists, somewhat confused, begin to re-examine what money actually is. The monetarist school developed during this period.

To this day, many economists still emphasize the superiority of commodity money. These economists rarely recognize Bitcoin, because in their view Bitcoin is not a commodity and has no use value in itself.

After all, gold has industrial uses and can be used for decoration. What can Bitcoin be used for?

Fiat money does not have the use value of commodity money, nor can it be rigidly converted into collateral the way gold-standard money could. But economists who support fiat money are even less likely to recognize Bitcoin, because fiat money is also supported by underlying value.

For example, a country’s currency is generally issued by its central bank. But a central bank does not simply print money. The money it issues is backed by assets. To examine these assets, one can look at the central bank’s balance sheet.

Generally speaking, these assets include various forms of debt, such as mortgages and corporate loans; equity assets, such as stocks; and foreign currencies, such as the U.S. dollar. These assets all represent the economic strength of the nation, such as its ability to repay debt.

In other words, fiat money is backed by the national economy. By contrast, Bitcoin appears to have no asset collateral behind it.

Therefore, Bitcoin has neither the use-value support of a commodity nor the collateral-value support of assets. Therefore, Bitcoin has no value. Therefore, Bitcoin must soon go to zero.

The logic of these economists sounds highly reasonable. But as described in the first part of this article, their judgment is based only on the more common monetary systems they have observed.

Ironically, before the birth of today’s fiat-money system, no economist believed it was reliable. If President Nixon had not “defaulted” by forcibly severing the dollar’s link to gold, we would not have today’s monetary system.

These experts usually believe that anything inconsistent with existing theory cannot work. But looking back at history, there are many examples that completely violated their theories yet truly existed.

Before Bitcoin appeared, had there ever been a currency that had neither practical use value nor asset collateral backing it?

Of course there had.

The Prototype of Bitcoin

The stone in the image above was money.

Several hundred years ago, on a small island called Yap, islanders used these stones for transactions.

Do not underestimate these stones. Many major figures in modern economics studied them. For example, Milton Friedman, one of the founders of monetarism and a figure comparable in importance to Keynes, once wrote a paper studying these stones.

The stones were extremely large, sometimes weighing more than a car. Villagers had to expend enormous effort to transport one stone from another island.

You might ask: how could this money be carried?

The answer is: it did not need to be carried at all. These stones simply stayed where they were. The villagers were orally informed about who owned each stone.

Whenever a transaction occurred, everyone in the village was orally notified that ownership of the stone had changed hands.

Even more strikingly, people did not even need to see the stone to recognize its existence and use it in transactions.

These stones were transported by villagers from another island. Once, a villager’s boat capsized in a storm and the stone sank into the sea. But the other villagers believed the stone existed. As a result, the stone continued to be used as money.

The island still exists today. Although residents now use the U.S. dollar as their common currency, the stones are still used as money on special occasions, such as resolving major disputes.

Milton Friedman

The Essence of Money

Did these stones have commodity use value? No.

Did they have asset collateral behind them? No.

Then why could they become money? What do they have in common with gold and fiat money?

The answer is simple: people believed they could serve as money. In other words, people reached a consensus that these things could become money. That is the most essential reason they functioned as money.

This is why so many types of money have appeared throughout history. Some were commodities. Some were backed by collateral. Some were nothing at all. These forms are not necessary conditions. They were chosen, or abandoned, only because people selected better objects around which consensus could be formed.

Of course, consensus does require certain conditions.

Yap’s giant stones could generate consensus partly because they were scarce — they required great effort to produce and transport — and durable, meaning they would not rot or disappear quickly. These features made people recognize them as suitable attributes for money. More importantly, the village’s consensus around the stones as money was difficult to destroy.

There were only so many people on the island. If someone tried to deny a debt, he would not be able to remain part of the community. If someone tried to flee with the money, first he would have to move the stone; and even if he could move it, where else could he use it?

Commodity money could become widely used because, in the corresponding environment, the consensus around it was difficult to destroy. Since the money itself had commodity use value, even if someone refused to recognize it as money, you could still use it as a commodity. That gave people a sense of security. This sense of security was the foundation of consensus.

Fiat money is the same. People’s trust in the national economy and government is not easily destroyed. In fact, all paper currency is built on trust in the state. If you do not trust the state, you will not trust that the state will honor gold-standard rules or asset-backed currency issuance. The state can default.

This is why fiat money must be issued by the state. The state is the most authoritative institution on which people rely to build consensus. After all, everyone depends on their country to provide basic welfare and security.

Moreover, fiat money cannot be rigidly redeemed. People accept renminbi or U.S. dollars not because they have carefully calculated the central bank’s balance sheet, but because they trust the country.

Therefore, many experts have seen the form of money, but have not understood the essence of money.

The essence of money is that it is used to conduct transactions. If something can fulfill the function of transaction, then it can be money. And for something to fulfill that transactional function, the necessary condition is that people must reach consensus that it can serve as money.

Bitcoin’s Characteristics

Can Bitcoin form consensus?

In theory, Bitcoin has all the conditions needed to form consensus.

First, because of its distributed ledger system, users do not need to worry about incorrect records or defaults.

Second, Bitcoin is scarce. Its total supply is limited and it is difficult to generate. It can also be stored permanently. It is not a physical currency and will never deteriorate or rot.

Third, Bitcoin is convenient to store and transact. In fact, compared with gold and fiat money, one can easily list many advantages of Bitcoin. Since this article assumes readers already understand Bitcoin’s functions, I will not elaborate further.

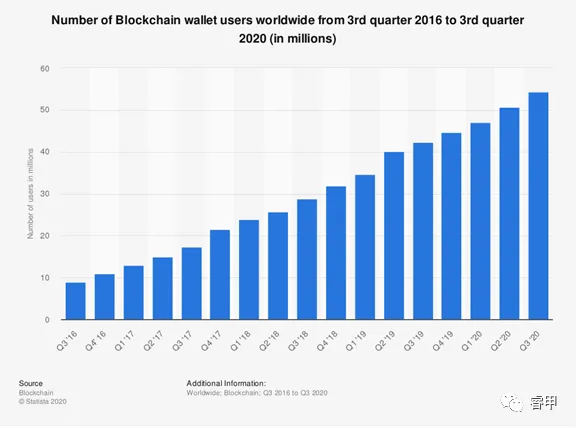

However, whether consensus can form is not determined merely by theory. It must be proven by facts. The past ten years have already shown that humanity has reached consensus around Bitcoin’s monetary function.

Like Yap’s giant stones, Bitcoin was initially used only within a small community — mainly among information-technology users. They quickly reached consensus on Bitcoin’s mechanism. Because Bitcoin could indeed perform the transactional function well, people used it more and more frequently, and the group of people recognizing it expanded rapidly.

Today, according to incomplete statistics, tens of millions of people globally own Bitcoin. Some merchants, including Starbucks and AT&T in the United States, have begun accepting Bitcoin payments. Bitcoin’s user base is growing rapidly.

But does this mean Bitcoin is already a mature currency?

Clearly not.

The most important criterion for judging whether a currency is mature is whether prices denominated in it are stable, or whether its price against another mature currency is stable. Bitcoin’s price relative to fiat currencies such as the renminbi or U.S. dollar is highly volatile.

Why is that?

The reason is simple: relatively few people still use Bitcoin for transactions. People are primarily accustomed to using fiat money for transactions.

Imagine that suddenly all fiat currencies in the world disappeared and everyone used Bitcoin as the sole currency for transactions. In terms of its attributes, Bitcoin satisfies all monetary functions, and it would immediately provide stable prices.

You might then ask: if we already have fiat money, we do not need Bitcoin. So why is Bitcoin valuable, and why has its price kept rising?

The reason is that the consensus foundations of Bitcoin and fiat money are different. To a large extent, the consensus foundations of the two are complementary rather than overlapping.

For example, fiat money is centralized. Bitcoin is decentralized by nature. Fiat money can be issued without limit. Bitcoin’s supply is limited.

In extreme situations, when consensus around fiat money collapses, Bitcoin may directly replace it. For example, during Zimbabwe’s hyperinflation, Bitcoin briefly became one of the main transactional currencies.

In a world where fiat money remains the mainstream universal currency, people’s consensus view of Bitcoin is not that it is redundant. Rather, they see it as an additional option, or a form of accident insurance.

It is similar to commuting: you can drive to work, or you can ride a bicycle. Most of the time, you choose to drive. But if traffic is severely congested, or if your car breaks down, you can choose the bicycle. Having an option is clearly better than having no option.

Given that Bitcoin’s price is still relatively unstable, people currently view Bitcoin more as a valuable asset to hold than as a currency. Yet it possesses all the attributes and consensus foundations of money and can be used for transactions.

Bitcoin’s Potential

At present, Bitcoin has a unique foundation of consensus. This gives it irreplaceable value.

Nietzsche famously said: “What does not kill me makes me stronger.” Bitcoin’s core holders and maintainers — including early Bitcoin investors and miners — have extremely strong faith in Bitcoin. Otherwise, we would not have seen Bitcoin reach new highs again after multiple drawdowns of 70%.

As more people buy Bitcoin as a store of value, and as it is used more frequently in daily transactions, its price will become increasingly stable. In fact, over the past several years, Bitcoin’s volatility has gradually declined. But in terms of actual users and usage scope, Bitcoin is still at a very early stage.

Bitcoin 30-Day Volatility

To judge Bitcoin’s long-term price trend, we should look at supply and demand based on economic principles.

Bitcoin’s supply side has already been predetermined. There will never be more than 21 million bitcoins in the world. But the demand side still has enormous room to grow. Demand mainly comes from two areas: demand for consumption as money, and demand for asset allocation.

As money, as long as national fiat currencies remain stable, Bitcoin will necessarily remain only a secondary option. However, the blockchain technology underlying Bitcoin gives it unique advantages in cross-border transfers and transactions. For example, transferring money from the United States to the United Kingdom may take a day, whereas Bitcoin can be much faster.

PayPal, one of the world’s largest mobile-payment platforms, recently announced that it would allow users to freely exchange Bitcoin and use it in 2021 for purchases at the 26 million merchants supported by PayPal. This is the first time Bitcoin has been accepted as a universal currency by a major mainstream payment platform. In this scenario, it is easy to imagine users using Bitcoin to buy goods from countries around the world. While this will not replace fiat money, it will greatly promote Bitcoin’s adoption.

By comparison, demand for Bitcoin as an asset allocation by investment institutions will be much larger. Compared with fiat money, Bitcoin’s greatest advantage is its inflation resistance. In this respect, it is fundamentally similar to gold, which is why Bitcoin is often called digital gold.

At present, however, Bitcoin’s market capitalization is almost negligible compared with gold. In my earlier article, Asset Valuation, Monetary Expansion, and Value Consensus After the Global Pandemic, I explained that if Bitcoin were to reach one-third of gold’s market capitalization today, its price would have to rise by at least 30 times. Once Bitcoin ETFs are adopted, the access channel for institutional investors will be fully opened, and Bitcoin’s market capitalization will inevitably rise rapidly.

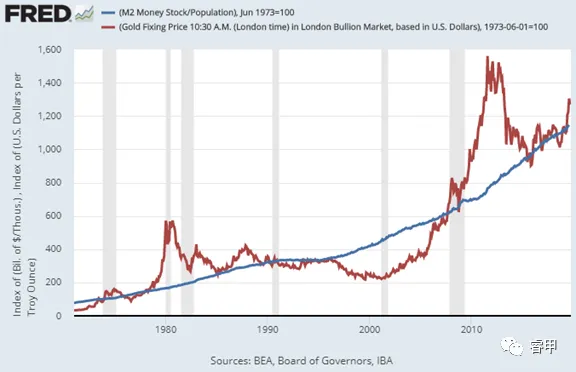

Over the past 50 years, gold’s annualized return has exceeded 7%. The chart below shows gold prices relative to the U.S. M2 money supply. Although gold prices are affected by changes in supply and macroeconomic factors, we can see that gold and M2 have risen roughly in tandem over the long run. Against the backdrop of global low interest rates and large-scale money creation, it is foreseeable that M2 supply will continue to increase substantially.

Compared with gold, Bitcoin is even more inflation-resistant, because gold can be continuously mined, and in the future it may even be mined in outer space. In fact, the total amount of gold mined over the past 30 years has doubled. Bitcoin’s total supply, by contrast, is fixed, and nearly 90% has already been mined.

Some people argue that Bitcoin holders may not have the same “holding power” as gold holders, because gold holders include government institutions such as central banks. This view exaggerates central-bank ownership. Based on Wikipedia’s 2011 data, central banks held only 17.2% of the world’s total gold supply. Most gold is used as a commodity, investment product, or industrial material.

Of course, no one can guarantee that central banks will not buy Bitcoin in the future. At the very least, large institutional investors have already begun buying Bitcoin.

According to a Fidelity survey, 25% of institutional investors in Europe and the United States — including pension funds, family offices, investment advisers, and hedge funds — have already begun holding Bitcoin. According to a September survey by the insurance company Evertas, 90% of these institutions plan to increase their holdings in the future.

Risks of Holding Bitcoin

The first risk is market-structure risk.

For any currency, ownership distribution follows a power-law distribution: a very small number of people hold most of the currency. In plain language, they are the “market makers” that influence price.

For fiat currencies, the dominant players are national central banks and giant investment institutions. For Bitcoin, they are mining pools and early investors. For example, records show that mining institutions currently hold about two million bitcoins.

Because Bitcoin’s dominant holders are not government institutions, their buying and selling behavior is relatively random. In an environment lacking regulation, dominant holders can more easily manipulate prices. Therefore, for quite some time, Bitcoin will still face the risk of sudden large price swings.

However, as long as no event occurs that damages Bitcoin’s foundational consensus, the probability of collective selling by dominant holders will become lower and lower.

At the same time, research shows that over the past several years, Bitcoin has been moving from large holders to smaller holders. According to Bitcoin.com, over the past five years, the share of total Bitcoin held by accounts with fewer than 10 bitcoins increased from 5.1% to 13.8%.

Given the large influx of users into the Bitcoin market, this is not surprising. Over the long term, as the ownership share of large holders gradually declines, Bitcoin’s volatility should continue to fall.

The second risk is physical risk.

Bitcoin wallets can be stolen or lost. But this is a human risk that can be prevented and avoided. I will not expand on that here.

The most fundamental risk of holding Bitcoin is whether its consensus foundation could be destroyed. At present, no substitute for Bitcoin’s consensus is visible. But future technological developments, such as quantum computing, could threaten Bitcoin’s rules.

In this respect, we must trust the strength of the Bitcoin community. Bitcoin is maintained by a community and team that are among the most knowledgeable in computer and internet technology. If a technology emerges that could damage the existing Bitcoin network, the community will respond and prepare in advance.

In fact, if such a technology emerged, it would likely first threaten traditional monetary networks. Bitcoin’s system is relatively much harder to break. That gives the Bitcoin community more buffer time.

Conclusion

Bitcoin is an immature currency, but it is also an inflation-resistant asset. Its network system is already mature, while its use cases are only beginning to open up. Therefore, compared with assets such as gold, it has enormous appreciation potential, but it also carries higher risks.

Since the COVID pandemic, expected returns on assets and the value of currency have both been discounted. Readers interested in the details may refer to my earlier article, Asset Valuation, Monetary Expansion, and Value Consensus After the Global Pandemic. In such an environment, holding some Bitcoin can at least serve as a hedge against traditional assets.

However, given the uncontrollable risks associated with Bitcoin as a non-government-supported network, we do not recommend that investors make Bitcoin a primary asset allocation at this stage. Generally speaking, Bitcoin should remain below 10% of an investor’s total assets, and should be held on that basis for the long term.

Author Biography

Yijia Fan is the founder and managing partner of iOne Capital Management.

iOne Capital is a U.S.-registered investment management firm providing asset management services to global high-net-worth clients.

Company website: https://ionecap.com

Legal Disclaimer

This article is original content and may not be reproduced without permission. The views expressed herein are solely those of the authors. This article is provided for informational purposes only. Even if the views expressed change in the future, the authors have no obligation to update this article.

This article does not constitute an offer to sell, a solicitation to buy, or a recommendation to trade any securities. Its sole purpose is to provide information and perspectives. Nothing contained herein should be construed as financial or investment advice on any subject.

The authors assume no responsibility for any actions taken by readers based on any information contained herein.