1. The Worst and Best of Times

In the first half of 2022, U.S. equities experienced their largest first-half drawdown in the past 50 years. U.S. bonds, meanwhile, suffered their largest drawdown in more than 200 years.

Everywhere one looked, the outlook seemed bleak.

Inflation was at its highest level in decades. Consumer confidence had fallen to levels last seen during the 2008 global financial crisis. The Federal Reserve was still raising interest rates. Across the media, a large number of investment experts and industry leaders were discussing the reality and outlook of recession. The only disagreement seemed to be whether the future would be “bad” or “very bad.”

Just as investors become increasingly optimistic during a bull-market upcycle, they become increasingly pessimistic during a bear-market downcycle. That psychological process usually begins with doubt, turns into anxiety, and ultimately becomes despair.

By “despair,” I mean the belief that the future world will enter a completely different and worse “regime” or “paradigm,” and that this new regime will persist for a long time.

We often hear such views from well-known investment institutions or influential investors.

So far this year, almost all major investment institutions — including Blackstone, Bridgewater, KKR, and others — have issued varying degrees of similar pessimistic commentary. The core message is roughly this: the global order has undergone a major negative shift, and the world has entered a new chapter.

Let us put aside, for the moment, whether these judgments are correct. The more important question is: should investors make investment decisions by following the views of these major institutions and prominent investors?

To answer that question, one must first recognize a subtle fact: by the time these institutions and experts make such statements publicly, they have usually already significantly reduced exposure, exited positions, or established short positions. Otherwise, they would not release such messages. And if they change their views later, they usually will not tell you immediately.

No one holding assets will tell others, “I’m bearish, you should sell first,” unless they are trying to mislead you so that they can buy at lower prices after you sell.

In other words, when the overwhelming majority of institutions and experts are bearish, it often means the market’s major capital has already exited — and may even be using leverage to short the market.

In several previous articles, including Is Now the Time to Invest in Technology Growth Stocks?, I have mentioned that whether we look at recent institutional-investor sentiment surveys or actual selling data, investor positioning has already reached its lowest level since 2008. In some data series, it has reached a 30-year low.

In fact, even retail investors — who are usually the least informed and the easiest to be hurt by market timing — have already fled the market. Fundstrat data suggest that in June, retail outflows reached their highest level since 2008.

In theory, the future can always get worse. Therefore, markets can always continue to fall. Trying to identify the exact turning point in the short term is almost impossible.

But over the long term, when investors collectively enter the stage of despair, it is usually a good time to buy.

Let us look at several notable examples from the past four decades.

In June 1981, in order to suppress the long inflationary wave that had lasted throughout the 1970s, the Federal Reserve raised interest rates from 10% to 20%. This triggered a recession, and the S&P 500 fell by 20%.

At the time, both major investment institutions and the public believed the Fed had made a grave policy mistake and had pushed the U.S. economy into a new and unknowable “regime” of endless darkness.

Yet after the S&P 500 bottomed in 1982, it rose more than 200% over the next five years through 1987.

In October 1987, for reasons that still cannot be fully determined, all 23 major global financial markets suffered sharp declines. The famous Black Monday occurred. The S&P 500 fell 30% in just two months. At the time, all major investment institutions collectively believed that the global financial system had suffered a systemic collapse and that the world’s financial network would enter a new dark “regime.”

The White House even invited the world’s top economists to form an expert team to analyze the future of the economy and markets. This group of elite experts reached a collective conclusion: the outlook for global markets over the next ten years would be extremely bleak.

Yet beginning in 1988, the S&P 500 entered a 12-year super bull market. It reached a new high in just over one year, and the next decade delivered returns of roughly 300%.

In 2000, the IT bubble that had accumulated over several years finally burst. The Nasdaq had risen more than fivefold over the previous five years. Combined with 9/11 and a series of other disastrous events, this led to a bear market lasting more than two years.

By 2002, all institutional-investor sentiment surveys were at historic lows, as if investors believed the information-technology revolution had merely been a fantasy. For example, according to Bank of America’s global fund manager survey at the time, allocations to technology stocks reached historical lows, and a significant share of investors were short.

Yet over the following 20 years, the Nasdaq 100 rose more than 1,000% — a more than tenfold gain.

In 2008, the global financial crisis erupted. At the time, almost all top institutional investors told clients: go home and sleep — the world had entered a new chapter, the future would be dark, the global financial system would never recover, and a once-in-a-century depression had begun.

Yet if you had bought the S&P 500 just one month after Lehman Brothers collapsed, you would have achieved returns of more than 10% over the following year. By today, your return would exceed 300%.

In 2020, the COVID crisis swept across the world. We all know what happened afterward. If you had bought U.S. equities one or two months after the crash, your return by now would still exceed 40%.

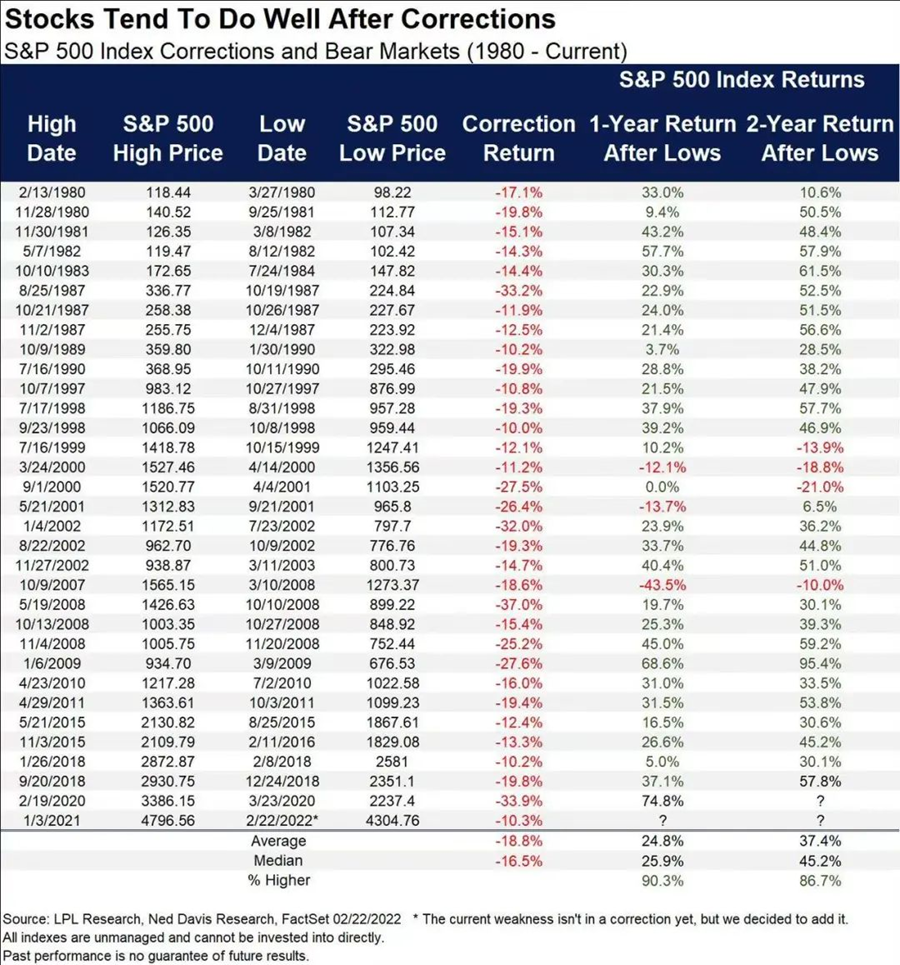

The above are all examples of sharp market crashes. In previous articles, we showed the one-year performance after every S&P 500 correction of more than 10% since 1980. The chart is reproduced below.

Since 1980, the S&P 500 has experienced 33 corrections. In the following year, the market rose roughly 90% of the time, with a median gain of more than 25%. The periods that did not produce gains were the 2000 IT bubble collapse and the 2008 financial crisis. We will discuss these two cases separately later.

One might say: how could I possibly buy at the exact bottom? Of course, that is impossible. But here is the remarkable point: even if you bought at the market peak before the decline, there is still a high probability that you would have generated positive returns within one or two years — and the returns were often not small. Readers can verify this through simple calculations.

In other words, as long as you can hold through volatility, even if you absorb every decline, the final outcome is far better than repeatedly selling or stopping out during every drawdown.

Perhaps this explains why most institutions that like to set “stop-loss lines” underperform the market over the long term. In fact, precisely because most long-biased institutions like to set stop-loss lines, most of them fail to outperform the S&P 500 over long horizons.

Every time we are near the bottom of a bear market, we feel as though “the future will never get better” and “the world has permanently deteriorated.” At that moment, we can always find a hundred convincing reasons to support that feeling.

During every crash, are there dissenting voices? Of course. But such voices are usually not mainstream, or they are easily ignored.

If we think about it in reverse, this is easy to understand: if optimistic voices were mainstream, the market usually would not be at the bottom. In that state, bullish and bearish forces would still be interacting, and the market would not be one-sided.

2. Cognitive Limits and Bounded Rationality

Let us return to the earlier question: when market sentiment is extremely pessimistic, is the collective consensus of major institutional investors usually correct?

I believe their analysis and understanding of the present are often correct. But historical experience shows that almost no expert or institution can consistently and precisely predict how the future world — especially financial markets — will evolve.

I previously wrote a dedicated article on humanity’s ability to forecast the future, How Should Investors Forecast the Future? Interested readers may refer to it.

This raises the question: if we can understand the current state of the world quite well, why can we still not accurately predict the future?

The logic is simple. Each of us can easily understand today’s weather. But predicting the exact weather one week from now is much harder.

Financial markets are far more complex. Broadly speaking, our ability to predict the future is extremely limited for several reasons:

- The world contains too many variables. As human beings, we only have access to limited information and data. Our brains have limited capacity to process that information. Therefore, we are destined to focus on and understand only a subset of variables.

- Even among the variables we can understand, it is difficult to determine how they will evolve in the future, because many of the underlying variables affecting them may themselves be hard to grasp.

- Human beings have innate biases, whether conscious or unconscious. These biases lead us to focus on some variables while ignoring others. When we are optimistic, we ignore negative variables. When we are pessimistic, we ignore positive variables.

- Some variables are not visible today, or do not even exist today, but may appear or be created in the future and may ultimately dominate the direction of the world.

- Our responses to the present world influence the direction of the future world, and those effects are themselves difficult to predict.

For example, when the 2008 financial crisis erupted, people focused on the state of the financial system at that moment to judge its future evolution. But very few people anticipated that the Federal Reserve would use quantitative easing to support financial markets.

Of course, almost no one anticipated that Bitcoin would be born as a result.

When the COVID crisis erupted, people focused on the damage lockdowns would cause to economic activity. But very few people simultaneously focused on the types of economic activity that would benefit from lockdowns, such as stay-at-home consumption, online consumption, and communications. Even when people did notice these sectors, they often underestimated their contribution to the overall economy.

Consider the current environment. If the recession that everyone fears begins to occur, inflation would likely decline significantly. In that case, the root cause of the recession would no longer exist, and the Fed’s rationale for raising rates would also no longer exist. The economy could then recover quickly.

If markets have already priced in recession expectations by that point, then when recession signals become obvious, markets may already begin pricing in the recovery. Asset prices could then recover rapidly.

Because of these dynamic and complex changes, precise forecasting is extremely difficult. Fortunately, we do not need to predict the future precisely in order to make good investment decisions.

An investment decision depends on two things:

- What the future will look like.

- What investors expect the future to look like, as reflected in asset prices.

Most investors focus too much on the first point and ignore the second. Historical experience shows that even if we cannot know exactly what the future will look like, when investors collectively fall into despair, the future usually turns out better than the collective expectation embedded in prices.

A large part of the reason lies in the limits of human cognition. When the macro regime changes significantly, people’s expectations for the future, as well as their behavior and reactions, tend to move toward two extremes: very good or very bad. Yet the future usually lies somewhere between those extremes.

Historical experience shows that the world is usually driven by alternating positive and negative variables. When conditions look bad, people overemphasize the negative variables and assume they will continue to dominate the future. Prices then incorporate that human reaction, while relatively ignoring positive variables that may influence the future — variables that may be hidden at the time, or may not yet have emerged.

It is precisely because of this cognitive bias that markets always have cycles. A cycle is not only an evolution of market participants’ emotions; it is also a process through which different variables alternately dominate the market.

Another reason is that human beings, as social creatures, inevitably constrain and influence one another. Especially at moments of crisis, behavior becomes highly correlated. Even if people recognize that the future may not be that bad, they may still take actions that appear irrational in hindsight — even though the logic behind those actions was rational at the time.

This may sound abstract, so let us use a practical example.

Assume you are a trader at an institution. A major world event has triggered clearly negative sentiment among most investors. The market is falling rapidly. Suppose that after rational analysis, you believe there is an 80% probability that the situation is not as bad as people think. But you also know that traders at other institutions are selling assets. What would you do?

Your firm evaluates your performance annually. If you hold your positions or add exposure, at least in the short term, your assets may face a larger drawdown. If you are wrong — even temporarily wrong — while everyone else is temporarily “right,” you risk being fired by your boss.

If you follow everyone else and sell, then even if your eventual performance is worse than the benchmark, others will be in a similar situation, and your risk of being fired will decline significantly.

So after rationally weighing the situation, you decide that keeping your job comes first. You choose to sell along with everyone else.

For an investment institution, the logic is the same. To satisfy clients’ psychological need for “risk control,” you are usually required to reduce positions or stop out.

This means that stop-loss rules can actually crystallize risk permanently. But persuading investors to accept drawdowns, or to go against the crowd in difficult times, is much harder. After all, they are not the ones managing the portfolio — you are. You cannot expect them to trust you as much as they trust themselves.

And at such moments, they may not even trust themselves.

These examples are very real. In fact, in MIT’s public graduate course on portfolio optimization, which is available on YouTube, a professor with many years of Wall Street trading experience explicitly tells students: “On Wall Street, the optimal trading decision is to make the same decision as everyone else.”

People often say markets are “irrational.” To some extent, this is not pure irrationality. It is rational irrationality — or, more precisely, bounded rationality. Market participants optimize locally according to their own needs, but the result does not lead to global optimization. It may even produce the opposite outcome.

Compared with large institutional investors managing enormous pools of capital, individual investors often have greater freedom in such moments, and therefore may face better opportunities. You do not need to be a top economist or analyst to recognize this.

3. The Deeper Logic of Contrarian Investing

Does this mean that every time markets collectively fall into despair, buying will generate excess returns?

For the S&P 500, over the long run, the answer has indeed been yes. But in the short term, not necessarily.

In fact, even during the worst period of the past century — the Great Depression of the 1930s — if you had bought during the depressed years of 1932 or 1933, your returns over the following three to four years would still have exceeded 100%.

This raises another question: this may be true for the S&P 500, but it is not true for every market. Japan’s market and some developing-country markets are examples. How should we explain that?

This touches on a deeper question: what necessary conditions must an asset satisfy for us to maintain long-term optimism toward it?

This is actually the most important and most fundamental question in investing. I believe this is the real factor that determines an investor’s long-term absolute performance. In our view, investors should spend more than 80% of their time during the investment process on this step — not on what to do after buying.

The answer directly determines whether investors have the courage to buy during crises rather than sell like most people. Over the long term, what often determines an investor’s performance is whether he or she can stay calm during moments of crisis.

I do not think there is a simple framework that can answer this question. It requires case-by-case analysis based on the nature of each asset. The correctness of your answer depends on the depth of your understanding. But we believe investors should focus on the underlying, structural, and difficult-to-change fundamentals that make up an asset’s long-term value.

For example, the long-term upward trajectory of the S&P 500 may depend on several conditions:

- Can the United States maintain an open, inclusive, optimistic, and innovative culture? Will entrepreneurial risk-taking and freedom continue to be respected and rewarded?

- Can the U.S. institutional and legal system preserve the basic principles and characteristics of a free-market economy, while ensuring that corporate operations and financial markets remain relatively fair, transparent, and efficient?

- Can the U.S. equity market reflect the growth and accumulation of the country’s primary monetary, wealth, and economic assets?

- When the country faces major crises, can the interaction between U.S. institutions, culture, and citizens expose these problems publicly and promptly, and generate open debate and correction?

These are merely my personal views. Different people may list different conditions. For other countries, such as China or Japan; other industries, such as new energy, high technology, or cryptocurrencies; or individual companies, such as Google or Alibaba, investors need to deeply understand and think through their underlying structural characteristics before making investment decisions. They need to list such conditions. In our investment framework, these are called an investment’s foundational conditions.

To engage in long-term investing, one must carefully think through these conditions and hold a positive view of them. Once one begins to doubt them, caution becomes necessary. The strength of your conviction depends on the depth of your understanding of the asset’s foundational conditions.

These foundational conditions are abstract rather than specific. Consider this analogy: if you were asked to make a long-term investment in a person, would you care more about that person’s achievements over the past year or the next month, or about the traits that could lead to long-term success — such as rationality, diligence, decisiveness, and patience?

When a major crisis erupts, the first question we should ask is whether the foundational conditions of the investment have changed. If they have not, then we should not sell the asset easily. If you can anticipate the crisis and sell in advance, of course that is ideal. In the final section, we will briefly discuss the characteristics of major crises. But historical experience shows that this is also extremely difficult, and we will discuss it further in the future.

At this point, some readers may say: is this not also forecasting the future? If one cannot forecast that the future will improve, one would not choose to invest. This method is simply less specific and less precise than most forecasts.

That is correct. Investing inevitably involves forecasting. The key question is whether you focus more on short-term, specific, and precise changes, or on long-term, abstract, and broad direction. Do you want to be precisely right every time, or broadly right over the long term?

The former involves many dynamic variables, and they are different each time. It is highly random. The latter involves fewer and more stable variables, and they remain more consistent over time. In fact, from the perspective of the latter, most variables involved in the former are just temporary noise. Therefore, consistently succeeding at the former is far more difficult than succeeding at the latter.

But judging the latter correctly is also not easy. At minimum, it requires investors to think deeply, and to possess extraordinary patience and willpower — to hold the line in dark moments, look through the fog, and wait for a brighter future.

4. The Characteristics of Deep Bear Markets

Let us return to the S&P 500 performance data after each correction of more than 10% since 1980. Two deep bear markets lasted more than one year each: the 2000 IT bubble and the 2008 financial crisis. In both cases, the S&P 500 did not perform well in the one to two years following the initial drawdown.

Therefore, buying immediately after every market decline does not always work right away. The future can always get worse, and investors may become increasingly desperate.

This raises the question: how can we identify a deep bear market in advance?

I believe we mainly need to consider the following factors:

- What is the key factor causing the market collapse?

- How extreme was that factor before the collapse?

- What was overall investor sentiment and positioning before the collapse?

- Did policymakers take timely and effective measures to contain further damage caused by those factors?

Generally speaking, the more destructive the factor causing the market collapse is to the financial system, the more extreme its magnitude, and the more euphoric investors were beforehand, the greater and longer the market collapse tends to be.

History shows that the following factors usually trigger deep bear markets:

- A debt crisis with major impact on the overall economy causes the market collapse.

- This type of debt crisis usually accumulates and compounds systematically over several years.

- Before the crisis erupts, most investors not only fail to recognize the risk, but are extremely optimistic about it, with speculative sentiment at unusually high levels.

- Policymakers ignore the risk, or fail to take timely action after the crisis erupts.

In short: the more intense the celebration, the more severe the subsequent collapse.

Both the IT bubble and the global financial crisis were caused by the bursting of massive leverage. In both cases, leverage had accumulated rapidly for at least five years. Before the crises erupted, leverage and price growth exceeded their historical averages by more than two standard deviations. Investors not only failed to stop, but became extraordinarily euphoric and believed the situation represented the future “new normal.”

In such a cycle, investor optimism always begins with real evidence, but ultimately ends in a fevered illusion. This does not mean that the industries driving the enthusiasm did not experience real development — technology, real estate, and the broader economy did indeed experience strong growth. But for a period of time, investor expectations ran far ahead of reality.

The Great Depression of the 1930s was one of the most severe financial crises in human history. Yet in the decade before it erupted, the United States experienced the “Roaring Twenties.” For more than ten years, the economy, culture, and social structure underwent one of the greatest advances and transformations of the entire twentieth century, ultimately leading to a feverish environment. Many readers may have read The Great Gatsby, which vividly depicts and foreshadows that era.

Of course, another reason the Great Depression became so severe was that policymakers failed to take timely and effective measures. By contrast, during the 2008 financial crisis and the 2020 COVID crisis, governments responded much more quickly and effectively, although those responses also created many negative side effects. In fact, part of the current difficulty we face is caused by the side effects of government stimulus policies.

Usually, for a deep bear market to occur, these conditions must be met simultaneously. Conversely, if the macro environment does not meet these characteristics, the bear market is usually shallower.

As a reference for readers, let us briefly compare these characteristics with the current U.S. macro environment.

First, the main reason for the market decline has been inflation, which has led to pressure from Fed rate hikes and economic slowdown concerns. During the market decline, emerging technology and growth assets were sold aggressively. However, we do not believe valuations in those assets before the decline reached levels comparable to the 2000 IT bubble. In fact, given the zero-rate environment at the time, valuations were not low, but they were not absurd either. Readers may refer to Is Now the Time to Invest in Technology Growth Stocks?

Although parts of the market contained high leverage and excess liquidity before the overall market decline — such as certain cryptocurrencies or meme stocks — they accounted for only a very small share of the market. The overall market decline was not driven by debt factors within those sectors, and those sectors do not have the ability to create a major negative impact on the overall economy.

Second, the factors causing the market decline did not undergo years of long-term accumulation or accelerating fermentation. Fiscal stimulus contributed to some inflation, but it was a one-off response to the pandemic. It was not a long-term stimulus cycle like the one seen in the 1950s and 1960s, so its impact is limited.

In fact, policy in the 1950s and 1960s was built for two decades around the mistaken belief that higher inflation would necessarily raise employment. That eventually led to a series of excessive debt expansions, a dollar crisis, and the long stagflation of the 1970s. The current situation is not comparable in scale.

Before the market decline, although equities rebounded rapidly and reached new highs because of abundant liquidity, we did not see the collective euphoria typical of a classic cycle peak. Instead, the market resembled a revenge rebound after artificial lockdowns created deflationary pressure and liquidity was then suddenly released. Many data series indicate that this rebound lasted only about six months and had already cooled by the first half of 2021.

In fact, the COVID crisis and high inflation kept household sentiment extremely depressed. The University of Michigan Consumer Sentiment Index never recovered to pre-pandemic levels after COVID broke out, and it worsened further beginning in the second half of 2021 — all before the major market decline.

Finally, while the Fed tightened relatively late, its pace was very rapid. CPI remains elevated, but prices of energy, real estate, and other assets; upstream industrial-production prices; and consumer-inventory trends already show that Fed policy has been effective. Most importantly, the factors that determine long-term sustained inflation do not exist. Readers may refer to Another Discussion on Inflation.

After substantial asset drawdowns and liquidity contraction, household and corporate financial conditions remain broadly healthy. Inflation expectations have also declined, and consumer sentiment has begun to recover.

Therefore, in aggregate, this bear market does not exhibit the classic characteristics of a deep bear market. Compared with previous episodes of “collapse after euphoria,” it is closer to a “normalization after distortion.”

We can never precisely predict where the market bottom will be. But by evaluating the present, we can understand whether the factors that triggered the bear market have weakened, or whether favorable factors are beginning to emerge. Comparing that assessment with prevailing market sentiment allows us to make relatively reasonable investment decisions.

Overall, I believe cautious optimism is the best investment mindset in a bear market. That is especially true in the current environment.

Author Biography

Dr. Yijia Fan is the founder and managing partner of iOne Capital Management.

iOne Capital is a U.S.-registered investment management firm providing asset management services to global high-net-worth clients.

Legal Disclaimer

This article is original content and may not be reproduced without permission. The views expressed herein are solely those of the authors. This article is provided for informational purposes only. Even if the views expressed change in the future, the authors have no obligation to update this article.

This article does not constitute an offer to sell, a solicitation to buy, or a recommendation to trade any securities. Its sole purpose is to provide information and perspectives. Nothing contained herein should be construed as financial or investment advice on any subject.

The authors assume no responsibility for any actions taken by readers based on any information contained in this article.