The following discussion is adapted from a November 7, 2025 conversation between two partners at iOne Capital. The conversation focuses on major asset classes — equities, bonds, gold, and Bitcoin — as well as real-time political developments, including the policy implications of New York City’s mayoral election and the Supreme Court’s review of Trump’s tariff policy.

Major Asset Classes

Liu: Let’s start with the major asset classes. First, equities. Recently, one of the key market debates has been the scale of U.S. technology companies’ AI spending. Many believe their investment has become excessive, creating a serious industry bubble — perhaps even comparable to 2000. How do you assess this risk?

Fan: I believe the risk remains manageable. To analyze this issue, we mainly need to look at two questions.

First, are these companies investing blindly and with excessive optimism? Second, are their investments excessive relative to their cash flow?

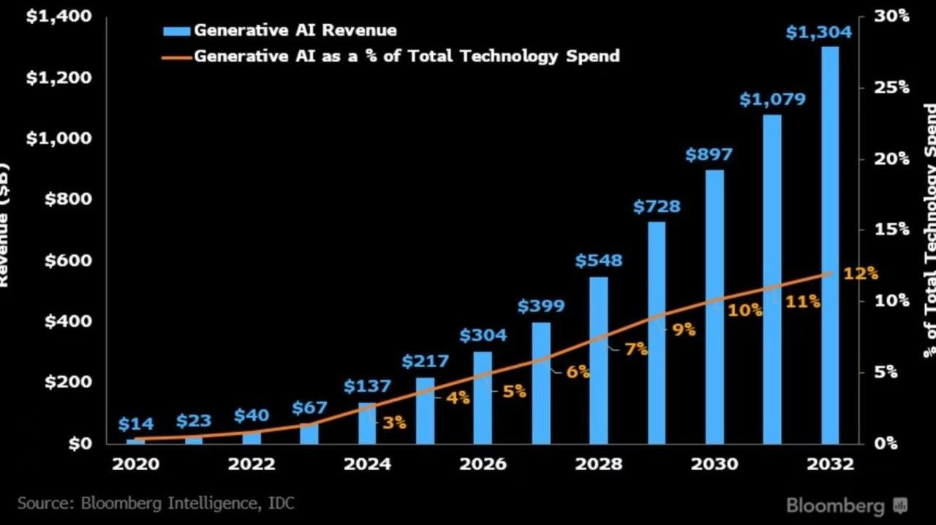

Let’s look at two charts. The first chart compares the trajectory of AI-related investment and output among the major technology companies. We can see that the two have moved largely in sync. In other words, these companies have increased investment as they have seen revenue increase, and they expect future AI-related revenue growth to significantly exceed the growth rate of AI-related investment.

Liu: So this is not irrational exuberance. It is a relatively rational capital-allocation decision.

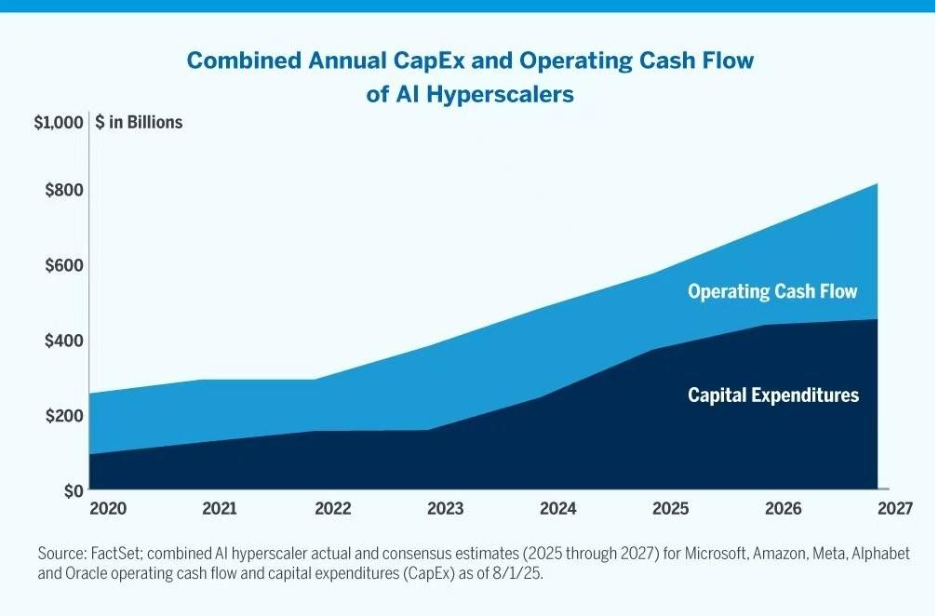

Fan: Exactly. Now let’s look at the second chart. We can see that AI spending by these technology giants is not only below cash flow, but also not particularly high as a percentage of cash flow. Moreover, over the next few years, that ratio is expected to decline further. So from a financial-position perspective, the risk is also manageable.

By contrast, at the peak of the IT bubble in 1999–2000, technology companies’ investment in internet and communications technology was completely disproportionate to the output being generated at the time. Most of the financing was also based on high leverage and borrowing.

Liu: From a sentiment perspective, today also feels different from 2000. At that time, there was far less public discussion about a bubble. Generally speaking, if everyone is worried about the same risk, that risk may actually be lower.

Fan: That’s right. As for the fundamentals and valuations of these companies, we have already discussed them in depth in the previous one or two episodes, so I will not repeat that analysis here. In short, we would still choose to continue holding exposure to the U.S. technology sector.

U.S. Small Caps and the Industrial Cycle

Liu: Apart from technology and the broad market, other areas of the U.S. equity market — such as small-cap stocks — have also been a focus for investors. The S&P 500 has delivered solid returns this year, but small caps have not significantly outperformed, which many investors had expected. How do you view the outlook?

Fan: Historical data and macroeconomic logic both suggest that small caps tend to outperform during economic recoveries. In most cases, that means falling interest rates and a rebound in industrial indicators.

In recent episodes, we discussed how the U.S. economy over the past year has gradually shifted from a rolling recession toward a rolling recovery. However, the shock from Trump’s tariffs, combined with the Fed’s decision to delay rate cuts in order to guard against inflation risks, has kept industrial indicators weak. As a result, although small caps have repeatedly shown signs of wanting to move higher this year, every time uncertainty has emerged, market confidence has been hit or delayed.

Liu: I have seen that industrial indicators have been weak for a record length of time. But these indicators are generally cyclical. Over the coming period, as the tariff impact diminishes or as rates fall further, should we expect a recovery?

Fan: Based on some of the leading indicators we track, yes. In previous videos, we mentioned that positive factors for the economy should become more dominant going forward, including the full implementation of the Big Beautiful Bill next year, further deregulation, and the realization of U.S. reindustrialization investment. All of these should support a recovery in industrial indicators.

More specifically, the data suggest that industrial indicators may recover over the next six months and reach a stronger phase in the second half of next year.

Of course, another factor affecting small caps is whether interest rates will fall further. That remains somewhat uncertain and depends on the pace of Fed rate cuts. But generally speaking, if the economy shows a clear recovery, even if the Fed slows the pace of rate cuts, that should not prevent these assets from rising. If the Fed decides to raise rates again, however, then we would need to reassess.

The Federal Reserve and the Inflation Outlook

Liu: How do you see the Fed’s rate-cutting path over the next year?

Fan: It depends partly on the level of inflation and partly on the nature of inflation. At present, the Fed appears relatively tolerant of tariff-driven inflation. At the very least, it is unlikely to raise rates for that reason.

By contrast, the greater risk over the next year may be inflation driven by economic overheating. In that scenario, Fed policy would become more uncertain, and we would need to monitor it closely. For now, however, that risk does not appear particularly high.

Liu: Third-quarter GDP and corporate earnings both looked strong. The economy appears to have meaningful momentum.

Fan: Yes, and that is consistent with our view at the beginning of the year. Over the next few years, investors need to focus on the three major structural forces driving this bull market: White House fiscal policy, the AI industrial revolution and domestic reindustrialization, and Fed monetary policy. At present, these forces appear likely to continue.

U.S. Treasuries: Why the “Collapse” Narrative Failed

Liu: How should we think about U.S. Treasuries? Over the past year, there has been no shortage of claims that the Treasury market would collapse. Yet not only has it not collapsed, yields are actually lower than a year ago. Among major developed markets, U.S. Treasuries have arguably been one of the best performers. How do you interpret this?

Fan: This is indeed an interesting phenomenon. It once again proves that investing is often counterintuitive. When everyone is looking in one direction, reality often does not unfold the way the consensus expects.

The first misconception among ordinary investors is that no one wants U.S. Treasuries anymore. This mainly comes from the grand narrative of so-called “de-dollarization.” But in reality, overseas institutional demand for Treasuries has continued to increase. We can look at the Bloomberg chart.

One point worth noting is that some governments may control their Treasury holdings for geopolitical reasons. But Treasury yields and prices are primarily determined by global market supply and demand. Government holdings are only one component. Moreover, government decision-making is not purely a price-discovery mechanism; it contains non-market logic. Overall market demand, including private-sector demand for Treasuries, continues to rise.

Another issue is that some data can be misleading. For example, some countries have not materially sold Treasuries, but have instead moved the custody location of their Treasury holdings overseas, which is not fully reflected in the statistics.

Liu: What do you expect over the next year?

Fan: The main factors are inflation, economic growth, and the direction of U.S. fiscal and monetary policy. The analysis is somewhat complex. But in aggregate, if the expansionary trend in the U.S. economy, fiscal policy, and monetary policy does not change, the probability of a sharp decline in Treasury yields is not high. The 10-year Treasury yield may remain in a 4% to 5% range.

If an unexpected event occurs, such as a financial-risk episode, then we would need to analyze it separately. Over a longer horizon, we will need to pay attention to the fiscal burden and whether the U.S. can maintain or reduce the debt-to-GDP ratio. We discussed that topic previously in our episode on Musk versus Bessent, so I will not repeat it here.

Gold and Bitcoin

Liu: How should we view assets such as gold and Bitcoin? Both have recently experienced meaningful pullbacks.

Fan: Our view on gold and Bitcoin has not changed. For ordinary investors, both are long-term accumulation assets. Unless one is a professional trader, we do not recommend excessive short-term trading.

From a fundamental perspective, gold still has value as a hedge against risk and geopolitical uncertainty, and as a hedge against the depreciation of all sovereign currencies. Bitcoin may generate higher returns than gold because, for large institutions, it remains an emerging asset with substantial room for growth.

Liu: Many people in the crypto community believe this cycle has already peaked. How do you view that argument?

Fan: Looking at previous crypto cycles, that argument does have some logic. But I believe this cycle is different.

On one hand, the macro fundamentals — including the economic cycle, monetary cycle, and liquidity environment — are different from prior cycles. On the other hand, institutional participation has changed the market structure. Compared with short-term traders, institutions are more likely to allocate based on medium- to long-term horizons.

From these two perspectives, my view is that in the short term, the crypto community’s ingrained “four-year cycle” mindset may lead to selling by crypto-native participants. But sustained institutional demand may provide support. Once the window associated with the so-called cycle peak passes, the logic of the macro cycle and medium- to long-term allocation should again dominate.

In other words, after a correction, Bitcoin is highly likely to continue rising rather than repeat the previous pattern of large boom-bust cycles that precisely matched the four-year halving cycle. In fact, the current price path already appears much smoother than in previous cycles, which has a great deal to do with changes in market-participant composition.

Liu: It sounds as though Bitcoin may be completing a transition from retail-driven ownership to institutional ownership, similar to gold’s early evolution.

Fan: That logic does exist. In summary, we recommend that ordinary investors maintain a low allocation but hold it for the long term.

Recent Market Volatility

Liu: Let’s look at recent market price action. Markets have experienced some volatility recently. What do you think has been the main cause?

Fan: The recent volatility has mainly been driven by anxiety over technology-company valuations and concerns about short-term liquidity tightening.

For example, several bank CEOs have publicly expressed concern about elevated U.S. corporate valuations. At the same time, because of the government shutdown, funds collected by the Treasury have remained in the government’s bank account instead of entering the real economy. In effect, this has withdrawn liquidity from the real economy.

In addition, bank reserves have recently become relatively tight, which has also tightened interbank funding liquidity. All of these factors have created pressure on the market.

That said, if we extend the time horizon to more than three months, these are short-term issues. As we discussed previously, technology companies’ innovation and earnings-growth capabilities are not in doubt. Any pullback is simply the result of short-term overbought conditions. After the pullback, the market should continue to rise.

The government is highly likely to reopen this month, which would release currently locked-up liquidity. If interbank liquidity tightens further, the Fed is highly likely to take measures to release liquidity, as it did in 2018.

Liu: Over the medium to long term, what is the biggest fundamental risk?

Fan: That is an excellent question. I believe the biggest risk over the next three to five years may be economic overheating, or the combination of an industrial-revolution-driven bubble and economic imbalances, eventually leading to recession — somewhat similar to 2000 or 2008.

Of course, one could say this type of risk exists at any time. But at present, the signs are not yet obvious.

New York City’s Mayoral Election and Policy Risks

Liu: We have covered major asset classes and the macro economy. Let’s now talk about recent U.S. political developments. The biggest recent news is that New York has elected a mayor who advocates socialist policies. I briefly reviewed his platform, which includes various free benefits, even free buses, government intervention to freeze rents, and even government-run supermarkets with price controls. He also proposed tax increases on corporations and high-income individuals, cutting police-department spending, and closing prisons. You have lived in the greater New York area for nearly 20 years. How do you understand the causes and consequences?

Fan: First, I deeply love New York City. I also fully understand why voters chose this mayor. Over the past several years, especially after the pandemic, New York has deteriorated in many areas — prices, public safety, and urban infrastructure. The previous two mayors failed to solve these problems effectively. Ordinary citizens are full of frustration.

During the campaign, this mayor accurately identified these issues and successfully channeled the public’s need to vent dissatisfaction.

But it is obvious that while he identified the right problems, the policies he proposed will not actually solve them. In the end, they will likely make the problems worse. I think investors watching our videos all understand the basic economics here, so there is no need to over-explain.

In short, economic imbalances are often caused by excessive government-policy intervention. Further intervention worsens the imbalance, and the public is then misled into demanding even more intervention. This creates a vicious cycle.

Liu: Can we also view the post-pandemic problems from a macro perspective? After the pandemic, there was a massive increase in money supply. People who owned assets benefited significantly. Those at the bottom were able to receive welfare support. But the working middle class has faced an increasingly difficult life.

New York, as a global city, attracts wealthy buyers from around the world, naturally pushing property prices higher. But the citizens who actually live there cannot simply leave at any time. This creates a structural imbalance, where they are forced to become the victims of monetary expansion.

Fan: That is indeed the case.

Liu: But I think real reform requires effective policies that remove barriers and allow everyone to share in the benefits of the market economy, rather than simply robbing the rich to help the poor or encouraging unearned benefits.

For example, on housing, the city needs to balance housing supply and demand, remove regulatory barriers, encourage more new housing supply, and raise limits on non-essential housing purchases. It should not suppress rents further and attack landlords.

If the cost of public goods is high, then the city should encourage private enterprises to participate in public infrastructure and prevent excessive expansion of union power. It should not fund “free” services by extracting more taxes from wealthy individuals and businesses.

Fan: What you said makes a lot of sense. But truly systematic reform has always been difficult. It requires leaders with wisdom, experience, and knowledge.

The flaw in the current U.S. electoral system is that the campaign process has increasingly taken on the characteristics of a reality show, rather than assessing candidates’ actual ability and experience in solving problems.

Liu: It is not easy to find leaders who can perform well politically and also govern effectively.

Fan: Exactly. In this environment, New York’s eventual transformation will require a collective awakening among the public. There are historical cycles here.

For example, in the 1970s, New York adopted policies similar to those of this socialist mayor and at one point essentially went bankrupt. Fortunately, it was rescued by the state and federal governments and later entered an upward cycle. After the pandemic, the city began declining again, and now it appears to have returned to another low point.

I believe New York will eventually move in a better direction, but it will take time. During that process, the city may suffer more pain.

Liu: I looked at voter statistics. Older voters mostly did not vote for this mayor. His support came mainly from young people, especially young women.

Fan: Yes. On one hand, older voters experienced New York’s earlier difficult period. On the other hand, this young mayor is personally charismatic, so it is not surprising that he attracted support from young female voters.

Of course, while New York’s situation is similar to that of some other cities, such as Chicago, it is not universal across all U.S. cities. In relative terms, some major U.S. cities are governed much better than New York. Miami is one example. San Francisco is another. After a long period of weakness, San Francisco now has a capable new mayor who has introduced effective policies. The city is currently recovering, and many companies and middle-class households are planning to move back.

Liu: How do you view the actual impact of the New York mayor’s policies, for example on the city’s finances?

Fan: If he fully implements the policies he promised during the campaign, then New York would almost certainly go bankrupt, and conditions across many areas would become more chaotic and deteriorate further. In reality, however, he may only be able to implement around 50% of his policies, and mainly the less damaging ones.

There are several reasons. First, he will face pressure from opposition forces in the City Council and from New York State. Remember, even in New York, he won with only 52% of the vote.

Second, when voters experience the negative side effects of his policies and provide negative feedback, he will seek balance. Therefore, I estimate that the probability of New York going bankrupt during his first term is still below 40%. But that is already a very high probability and absolutely cannot be ignored.

Supreme Court Review of Trump’s Tariff Policy

Liu: Another recent focus is the Supreme Court hearing on Trump’s tariff policy. How do you think the Supreme Court will ultimately rule on Trump’s tariffs?

Fan: I think the most likely outcome is that broadly applied tariffs on all countries — such as reciprocal tariffs — will be deemed illegal. But tariffs based on specific industry protection, or tariffs targeting certain countries for national-security reasons, are not especially controversial and will likely be preserved.

My judgment is based partly on prediction-market pricing, which broadly suggests that the Supreme Court will not side with Trump. It is also based on common sense.

When the Supreme Court makes a ruling, it must consider not only the current president’s case, but also the broader implications for future presidents. From that perspective, broad-based tariffs should not be defined as an emergency measure and should properly require congressional approval, or congressional legislation.

We have also seen that Congress’s recent position on Trump’s broad tariffs is very clear: it does not support what Trump is doing. So I believe the Supreme Court will side with Congress. Based on the questions asked by several justices during the hearing, they did indeed appear skeptical of the rationale for Trump’s reciprocal tariff policy.

Liu: That sounds like a significant impact. If that happens, would all tariff revenues have to be refunded? How large would the impact be?

Fan: If the Supreme Court rules that this portion of Trump’s tariffs is illegal, then that revenue would be refunded to businesses. Based on analyses from various institutions and AI models, as well as comments from Treasury Secretary Bessent himself, perhaps 50% to 70% of the tariff revenue could be refunded. Bessent has said that the White House has already prepared contingency plans for both scenarios.

Liu: That is a huge amount of money. If it happens, what would be the impact on capital markets?

Fan: The effects are complex.

From the perspective of the fiscal deficit, it would clearly increase the deficit because that revenue would be reduced. This could push Treasury yields higher, thereby affecting overall risk-asset valuations.

From another perspective, if those funds return to the private sector and tariffs are reduced, transaction costs for merchants and businesses would decline. That would be positive for companies and could increase net profits, supporting risk assets. In addition, inflation concerns would ease, reducing interest rates and financing costs, which would further support economic growth.

Overall, I believe that as long as the fiscal burden on the government is not too large, the net effect should still be positive.

Legal Disclaimer

This article is original content and may not be reproduced without permission. The views expressed herein are solely those of the authors. This article is provided for informational purposes only. Even if the views expressed change in the future, the authors have no obligation to update this article.

This article does not constitute an offer to sell, a solicitation to buy, or a recommendation to trade any securities. Its sole purpose is to provide information and perspectives. Nothing contained herein should be construed as financial or investment advice on any subject.

The authors assume no responsibility for any actions taken by readers based on any information contained in this article.